Trulieve Cannabis Corp - Jan 2023 Update

An updated look at the company moving into 2023

A lot has happened since we’ve written our last report on Trulieve. Events that most investors are familiar with include the failure of SAFE Banking to pass in the lame duck session of Congress, and President Biden’s instruction to the Secretary of Health and Human Services and the Attorney General to initiate the administrative process to review expeditiously how marijuana is scheduled under federal law.

Other developments in the Cannabis industry are present in day-to-day operations. Notably the downward pressure of flower prices in developed markets. Our latest monthly update on MA shows that prices have fallen to $229/oz in November, down from $377/oz a year prior and $399/oz when adult-use sales first started in November 2018.

In the financial markets, the sector’s sentiment is near rock-bottom. The big five multi-state operators have reached all-time-low valuations in December, and ETFs that track the sector continue their downward price trajectory.

We have taken into account the headwinds the industry faces and more over the past six months to provide an updated look at Trulieve going into 2023.

As mentioned in our previous report, though we aim to be unbiased, please note that we have an equity position in the company.

Company Specific Updates

We see four updates regarding Trulieve investors should be aware of moving into 2023.

Portfolio Adjustments for Future Profits

In a quest for profitability, the company decided to divest non-core assets. The statement came during Trulieve’s Q2 Earnings call in August by CEO Kim Rivers. In the second half of this year, the divestments included the discontinuation of Nevada wholesale operations and the closure of 2 dispensaries in California. Other divestments are possible as Trulieve looks to maximize cash flow in 2023.

Continued Expansion in Developing & New Markets

At the time of writing this report, Trulieve has expanded its retail footprint to 180 dispensaries. Including the addition of three dispensaries in WV, one in AZ & five in FL.

Along with retail development, the company made progress in expanding to new markets. This includes the announcement in September that Trulieve was officially awarded a Class 1 production license in Georgia. The license will allow Trulieve to operate up to 100,000 square feet of cultivation and up to 5 dispensaries to manufacture and sell low-THC oil.

The company also stated on its Q3 earnings call that they were awarded a cultivation license in Connecticut, which allows two adult-use dispensaries. The plans in CT include the construction of 24,200 & 35,200 square foot grow and processing facilities in Meriden and the relocation of their Bristol dispensary.

Though we did not include this in our last report, Trulieve was awarded an RFA II Provisional Dispensary License in May for a dispensary in Columbus, Ohio. The law states that license awardees have until February 2023 to start sales at the awarded location. We expect Trulieve to begin sales in the state in Q1 23.

Not a Trulieve expansion, but the citizens of Maryland voted to legalize the adult use of Cannabis during the 2022 mid-term elections. The bill states that adult use of Cannabis will become legal beginning in July of 2023. Though it is not clear how adult-use sales will roll out, there have been conversations regarding current medical operators converting to sell adult-use products in July. We had previously assumed that Trulieve would start adult-use sales in 2024; that remains our assumption given what we have seen in other states.

Debt Raised at Industry Leading Rates

Trulieve published two press releases in late December that unveiled a combined capital raise of $90.4 via secured commercial loans. The weighted average interest rates for the loans comes to 7.48%. The loan compares to competitor Verano Holdings refinancing a $350 million credit facility in October at a 12.75% floating interest rate.

Florida Facility Ramp-Up

The company has been very vocal about the state-of-the-art 750,000-square-foot cultivation and processing facility in Jefferson County, Florida, and have recently begun the ramp-up in the second half of the year. In Trulieve’s Q3 earnings call Kim Rivers commented that the company was able to maintain gross margins “due to increased utilization at our new Florida indoor cultivation facility”. Rivers also mentioned that the company “expect[s] the facility will be fully planted at the start of the year with initial harvest and optimization efforts continuing into the spring.”.

Moving forward, we see this facility as a way for Trulieve to sustain margins in Florida for the eventual price erosion we have seen in other states.

Financial Health

Trulieve’s Q3 financials have degraded since our overview of their Q1 numbers. Price erosion, lower-than-expected demand, and continued “digestion” of Harvest Health & Recreation are all factors.

Balance Sheet Metrics

High level, the Balance Sheet metrics are still healthy compared to Q1. We have highlighted lower cash levels, as these have decreased by $153 million since their Q1 filings. Trulieve’s $91 million in December debt raises will put cash back up to reasonable levels while maintaining a flat Debt-to-Equity Ratio.

Cash Flow Metrics

Overall, the company’s Cash Flow metrics for Q3 were poor. Negative cash flow was generated by negative operating income and compounded by $31 million of additional inventory, $16 million in accounts payable, & $28 million in tax payments.

During Trulieve's Q3 earnings call, management stated they “anticipate[s] operating cash flow will be positive in the fourth quarter, and we will generate free cash flow in 2023”. We expect cash flow to trend in the right direction moving into 2023, though our DCF assumptions still indicate negative FCFF in 2023.

Income Statement Metrics

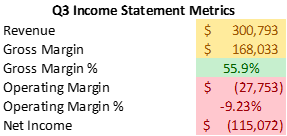

Revenue and gross margin declined from Q2 into Q3 by $20 & $14 million, as noted in the above chart. Kim Rivers stated the decline was due to “macroeconomic conditions, foregone revenue due to the strategic shuttering of non-core assets, regulatory changes in Florida, and the impact of Hurricane Ian” and points to a temporary decline in revenue that may pour over into Q4.

Gross margin continues to be the highlight of the income statement and remains stable over 2022, even with significant declines in revenue.

Asset write-offs hurt margins but should not be reoccurring moving forward. Analyst GAAP EPS for Q4 is -$0.09 / share, up from the current -$0.61 / share for Q3. Our view aligns with the consensus.

Risks

In addition to the risks we have previously highlighted, we wanted to highlight one additional risk.

Florida Adult Use Ballot

During the 2022 mid-term elections, four states had initiatives to legalize adult-use Cannabis, and the results were not as bright as advocates had hoped.

Two out of three red states ended up not legalizing adult use. Missouri passed the initiative, but with a small margin. These results make us more cautious regarding the possible Florida adult use ballot initiative passing in 2024. Especially since Florida requires all ballot initiatives to pass with at least a 60% margin, making it more difficult for voters to legalize Cannabis than in other states.

Future growth for Trulieve relies heavily on Florida cannabis converting from medical use to adult use, and likely why Trulieve has put $15 million into the program in the past six months.

Fair Value

Our updated DCF model gives us a fair value* range for Trulieve of $45.55 - $55.67 per share. A few of our original assumptions have changed in the past six months, and this value reflects those changes. The updates are as follows:

The leading factor in our fair value range change is that FL & PA are now assigned a 60% probability of converting from medical to adult use in mid-2025 and a 40% probability in mid-2029. Cash flows from each state were discounted accordingly.

Cannabis re/de-scheduling takes place in late 2024, causing the removal of the 280e tax code on Cannabis companies. Adds an estimated ~$165 million to FCFF in 2025.

We understand that the PA assumptions are conservative, but given the current climate we would rather be too conservative, than overly optimistic.

If our assumptions prove incorrect or there are further changes to the current outlook, our fair value range will need to be updated accordingly.

*Pink Horse Capital Research Fair Value is not a price target or a buy/sell recommendation. Fair Values are based on assumptions of future cash flows discounted at rates aligned with the current climate. Security prices may never trade in our Fair Value range.

Before there is too much excitement about our fair value range, re-read the risks section of our initial report as nothing forward-looking is certain. As new information comes to light, including quarterly earnings, we will update this report. Make sure to subscribe below to stay up to date on the latest!

Don’t forget to follow us on Twitter. Get real-time insights on the Cannabis sector and the market in general!