Trulieve Cannabis Corp. - A Titan in the Making

Diving Head-First Into The Big Green Giant

US legal cannabis expects to be a $100B market by 2030. With 2021 sales capping off at $27B, this represents a CAGR of 15.66% for the nine years that follow, which sets the stage for our first report in the sector, on the largest company in terms of revenue in Q1 2022, Trulieve Cannabis Corp.

The report on Trulieve is our first published report here at Pink Horse Capital Research, where we aim to publish our findings on small & mid-cap equities, the companies that most research firms don’t cover. Though we aim to be unbiased, please note that we do have a position in the company.

With that said, let’s get into it.

Company Introduction

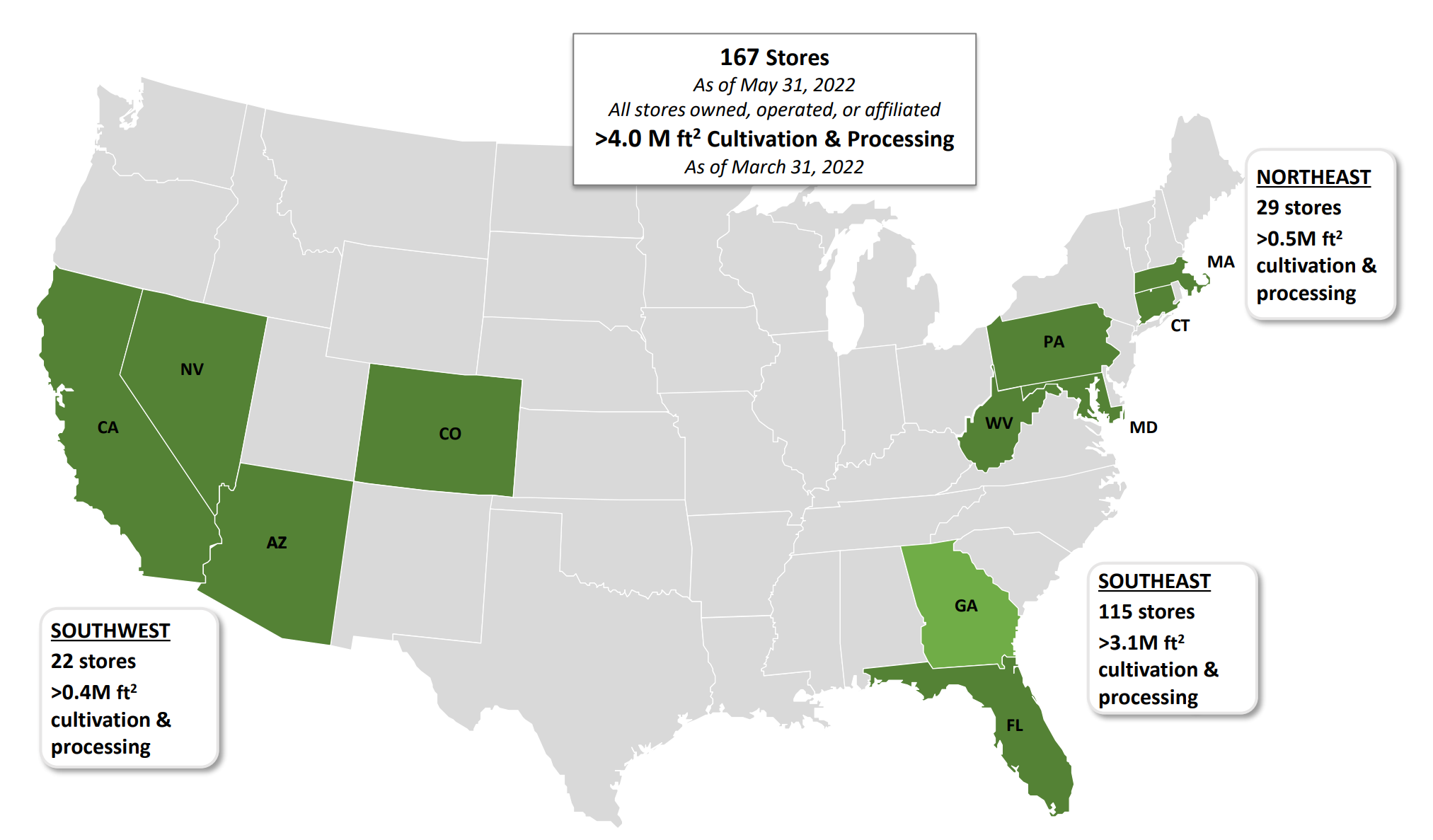

Trulieve Cannabis Corp. (referred to as Trulieve) is a vertically integrated, US-based, Cannabis company with operations in AZ, CA, CO, CT, FL, MA, MD, NV, PA, WV & GA. At the time of this report, Trulieve employs over 9,000 people, has 173 retail stores, and over four million square feet of cultivation & processing capacity.

Trulieve is led by CEO Kim Rivers. Kim is one of the founders and has been with the company since its inception. As of Q1 SEC filings, she was the largest single shareholder & owned 9.34% of Trulieve’s outstanding shares.

The company has an estimated 4.47% market share of the US legal cannabis market in Q1 2022. This is driven primarily by their large footprint in FL, where they have an estimated 42% market share of products containing THC and Cannabis Flower.

Trulieve had $318 million in sales for Q1 2022 & has given guidance of $1.3 - $1.4 billion for full year 2022. Sales of $1.35B for 2022 represent a 44% increase in sales year-over-year.

Business Model

Trulieve has a three-pronged strategy that is the guiding north star on how they operate their business. Below is an overview of each of these elements:

1. Scale in Market – While other large operators focus on a “land-grab” approach to the US Cannabis market, Trulieve’s first pilar focuses on scale within a state/market. The strategy is aimed to gain scale & market share to drive positive Net Income & FCF that funds future growth.

2. Vertical Integration – One saying we have heard Kim Rivers say on a repetitive basis is “Branded Product Through Branded Retail”. Another word for this is Vertical Integration. With Vertical Integration Trulieve looks to maximize margins by controlling the entire value chain. This unique legal quirk in the Cannabis Industry, where in many states this is required, differs cannabis from other traditional CPG categories. Trulieve looks to take advantage of this by using partner brands when possible, thus providing consumers with a variety of brand choices at their retail locations while avoiding excessive exposure to competitors’ products on their shelves.

These partner brands are brands that Trulieve grows & manufactures products for on behalf of the company. We believe that the brand partner gets a cut of the sale through a licensing agreement typical of a full-service approach within the CPG contract manufacturing industry. This approach is more profitable than selling competing brands in their stores.

Though Trulieve does supply products to the wholesale market, this is not their preferred path of doing business. Key to note in PA the company is currently at 100% wholesale penetration.

3. Hub Model – The company operates what they call a “Hub” model approach to Cannabis. With currently three Hubs (Northeast, Southeast & Southwest), Trulieve takes their “Scale in Market” approach and applies it on a regional basis around cornerstone states (PA, FL & AZ respectively). Kim Rivers has voiced she would like to have five regional hubs but has not stated details on the development of the remaining two.

Aside from building a brand & retail presence at a regional level, we see this approach as an intelligent way to scale their supply chain and sets Trulieve up for a future of interstate commerce (currently illegal without federal reform) and price compression. We believe the “Hub” model would allow Trulieve to supply its stores & wholesale from a single scaled location in that region. This approach is popular in price-sensitive FMCG businesses. For comparison, P&G operates 6 paper product manufacturing locations in the US in 6 “Hubs”. These include Oxnard, CA (Southwest), Bear River City, UT (Northwest), Green Bay (North Central), Cape Girardeau, MO (South Central), Albany GA (Southeast) & Mehoopany, PA (Northeast). The likes of AB-Inbev (Budweiser) & PepsiCo follow a very similar model for their beverage businesses as well.

Growth Story

We see the growth story for Trulieve broken out into 3 different segments, that correlate to the strategy that has been explained above.

1. Scale / Capacity Expansion In Current Markets

You don’t have to enter new markets if you can build out existing ones. The first growth driver is improving existing assets & building out where licenses allow driving sales. The two major drivers for Trulieve for this are:

Increased dispensaries & capacity/cultivation expansion in cornerstone markets (FL, AZ & PA)

Early investments in emerging Cannabis markets (GA & WV)

2. Entrance into New Markets

As mentioned earlier, Kim has noted the prospect of 5 Hubs. This would indicate that Trulieve is likely to expand the Hub model in the coming years to further geographic areas in the US. In more developed Cannabis markets, we would expect Trulieve to enter through M&A when the company finds attractive opportunities.

Though Trulieve is late to the party in key Northeastern states (mainly NJ & NY), we have seen the company focus its resources on more business-friendly states. This could indicate a strategy of entering developing markets closer to their home base in FL.

3. Medical to Adult-Use Cannabis

Cannabis legislation at the state level typically goes from allowing medical cannabis, then after some time, the state switches to adult use for those over 21. Early entrants to these markets are rewarded with large initial market share and margins before new entrants come in and the price compression cycle begins.

Trulieve is well positioned in two of its cornerstone markets of PA & FL to take advantage of the change once this occurs. Our analysis shows that in 2026, Trulieve’s revenue from these two states alone could be as much as $3.6 B. This represents ~3.5x the Q1 revenue run-rate we estimate the company makes from their operations in those states today.

Financial Health

A note about Trulieve’s Q1 financials. The recent acquisition of the distressed Harvest Health & Recreation has weighed heavily on its recent earnings. Statements from the company say that they are “digesting” the acquisition and expect metrics to improve in the future. Please note that no future-looking statements are certain.

With that, let’s look at some key metrics from the Balance Sheet, Cash Flow Statement & Income Statement below:

Balance Sheet Metrics

From a high level, these metrics display a healthy balance sheet, and there is minimal risk for the company to default on its debt or not pay its current obligations. There is also ample cash to make opportunistic investments should the right circumstance arise.

Cash Flow Metrics

Though operating cash flow & FCFE are good for Q1, the operating cash flow ratio tells us that in order for the company to succeed long term, OCF will need to increase going forward. FCFF is positive, but negligible for Q1.

Our DCF model does not account for Trulieve to become FCFF positive on a yearly basis until 2025, so we continue to expect low to negative FCFF until then.

Income Statement Metrics

Even with the gross margin compression Trulieve has experienced in the two recent quarters, 56% is still strong compared to other industries. P&G has a 48% Gross Margin (CPG), Diageo 61% (Spirits), Altria 67% (Tobacco), Ulta 39% (Specialty Retail) & Anheuser-Busch InBev 57% (Beer) on a TTM basis.

Operating margin has come down significantly recently, and we would like to see this normalize at least above 20%.

Net income continues to be negative but has improved drastically from Q4. Q2 analyst consensus is an EPS of $0.01, which would lead us to update the color coding in the above table.

Risks

There are two sections of risk as we see it with Trulieve. The Cannabis sector risk & company-specific risk.

Cannabis Sector Risk

With any emerging or growing sector with a high level of expected CAGR, there are substantial risks and should not be ignored by investors. Without getting into the weeds, the main risks for the sector include:

Legislative Risks - With the Cannabis sector heavily dependent on government regulation and approval to grow, the way the government decides to regulate, or the speed to which it does can affect the sector. The biggest concern is how federal regulations will look once they come into the picture. If legislation looks similar to alcohol, vertically integrated companies such as Trulieve may be forced to divest assets.

Illicit Market - The Cannabis black market is thriving and still accounts for the majority of sales in large legal markets. There are many factors at play as to why that is, but if the illicit cannabis market continues to thrive, this will eat into the legal player’s market share.

Not So Main Stream - Advocates in the industry are accounting for Cannabis to take alcohol, pharma & tobacco’s share of wallet, but what if this is not the case? In many circles, this is assumed as fact, though has yet to be proven on a large scale.

Company Specific Risks

One Hit Wonder - Trulieve has dominated the FL market with a proven ability to scale cost-effectively and have effective retail, but has not had the chance to show the same display of dominance in other markets. With Trulieve significantly expanding outside of FL in late 2021, 2022 & beyond will show if the company is capable of replicating its winning formula.

A Day Late & A Buck Short - The company is not present in key northeastern states, mainly NJ & NY, which will result in slower growth compared to peers. Being early in states before they legalize adult use can result in a large windfall during the first months/year of sales. Not being present can hurt performance. Though regulations in northeastern & western states tend to be less friendly to large cannabis companies. Time will tell if sitting out will hurt or help Trulieve in the long run.

Retail Heavy - Noting our sector risk, if federal legislation occurs that restricts cannabis companies from being vertically integrated, with 173 dispensaries, it would have a bigger impact on Trulieve than many of its peers.

Fair Value

Our DCF model has given us a fair value range for Trulieve of $79.30 - $96.92 per share. There are quite a few assumptions we took to arrive at this range, and if any prove incorrect, an update will be required. The assumptions with the largest impact are the following:

FL & PA go from medical to adult-use mid-2025. This assumes a Nov ballot initiative in 2024 that would provide the framework for Trulieve to sell to adults over 21 in the state.

FCFF turns positive at a 10% yield to revenue beginning in 2025.

Slower growth than peers in 2023 & 2024 as a result of not being in new adult-use states.

Trulieve maintains a significant market share in its cornerstone hubs in 2026, leading to a 9.18% US market share by 2030.

CAPEX reduction as a % of earnings continuing year over year.

Before there is too much excitement about our fair value range, re-read the risks section of the report as nothing forward-looking is certain. As new information comes to light, including quarterly earnings, we will update this report. Make sure to subscribe below to stay up to date on the latest!

Don’t forget to follow us on Twitter. Get real-time insights on the Cannabis sector and the market in general!

Nice overview, thank you. Would have liked to have seen you cover the 280e requirements that would be removed via legalization, and the big impact therefrom, as well as the capital markets access that would come with an uplisting opportunity. (Personally, I think we'll see a handful of acquisitions in the next couple of years that will bring Trulieve into new market areas and accelerate growth/profitability.)

ET

is your fair value based on the US ticker or Canadian ticker? (TCNNF or TRUL)?